Contents

With the Federal Reserve finally cutting interest rates, investors have a golden opportunity to consider adding dividend stocks to their portfolios. These stocks hold the potential to generate substantial returns in the coming years. However, it’s crucial to remember that a high dividend yield alone shouldn’t be the sole factor in your investment decision. Stocks that offer steady and growing dividends backed by solid business models are more likely to appreciate over time and deliver significant returns. Here, we explore three robust, high-yield dividend stocks worth buying now and holding for the next decade.

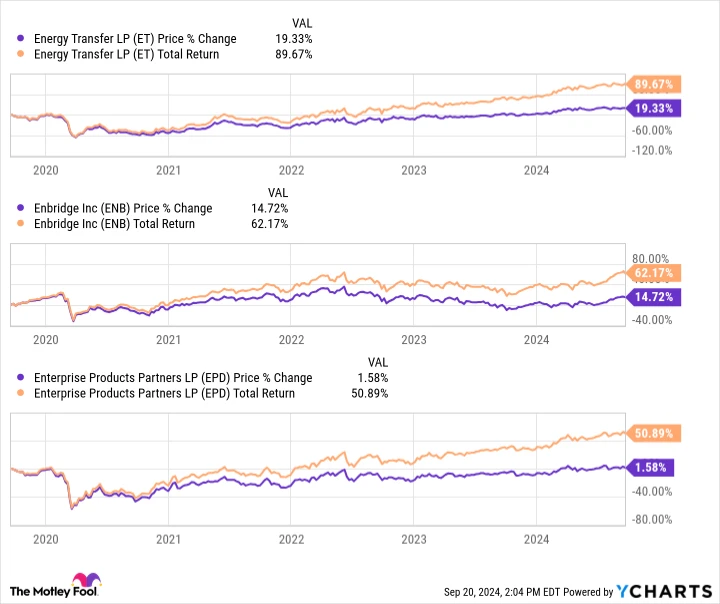

High-Yield Prospect No. 1: Energy Transfer

Energy Transfer (0.19%) emerges as a promising high-yield dividend stock, boasting an attractive dividend yield of 7.9%. Midstream oil and gas companies like Energy Transfer provide some of the most reliable dividends in the energy sector, thanks to their contract-based business models. While some may argue there are more well-known stocks with more robust dividend histories, Energy Transfer has outperformed its larger peers, such as Enterprise Products Partners and Enbridge, in recent years.

Energy Transfer’s Strategic Advantages

A significant portion of Energy Transfer’s revenue, approximately 90%, is derived from fee-based contracts, insulating it from the volatility of oil and gas prices. This stability allows the company to allocate a substantial share of its stable earnings and cash flows to its shareholders. Energy Transfer plans to distribute over 50% of its distributable cash flows (DCF) as dividends, invest up to 40% in growth, and use the remainder for debt repayment and share repurchases.

Energy Transfer’s acquisition of WTG Midstream Holdings for $3.3 billion is set to expand its presence in the Permian Basin. This acquisition, coupled with organic growth, should enable Energy Transfer to increase its annual dividend per share by 3% to 5% in the near term. Investors who purchase Energy Transfer stock now and hold it for a decade could see impressive returns, thanks to the combination of high yield and dividend growth.

High-Yield Prospect No. 2: Clearway Energy

The renewable energy industry is poised for rapid growth, with the International Energy Agency (IEA) predicting unprecedented expansion over the next five years. Investing in a renewable energy stock now and holding it for the next decade is a strategic move. Among the promising options, Clearway Energy (1.82%)(2.11%) stands out as an underrated high-yield renewable energy stock.

Clearway Energy’s Growth Trajectory

The IEA projects that solar and wind deployments in the U.S. will double by 2028. Clearway Energy, with a capacity of 9 gigawatts across 26 states, ranks among the largest renewable energy producers in the country, specializing in wind, solar, and energy storage.

Though Clearway Energy cut its dividend in 2019 due to a customer’s bankruptcy, the company quickly regained investor confidence by raising its dividend in 2020. It has consistently increased its dividend every year since. Through its affiliation with Clearway Energy Group (CEG), jointly owned by Global Infrastructure Partners and TotalEnergies, Clearway Energy accesses a robust pipeline of renewable energy projects for acquisition and growth.

Clearway Energy aims to boost its annual dividend per share by 5% to 8% through 2026. The company is already formulating its next cash-flow and dividend growth objectives for 2027, making its 6.2%-yielding stock an appealing long-term investment.

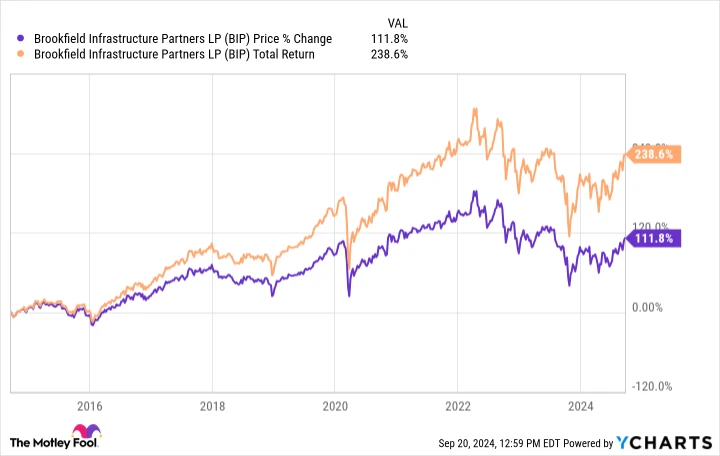

High-Yield Prospect No. 3: Brookfield Infrastructure

Infrastructure is the backbone of any economy, and investing in a diversified company with a strong portfolio of infrastructure assets is a savvy strategy. Brookfield Infrastructure (0.31%)(0.78%) is a standout choice for those seeking a reliable stock to buy and hold for the next decade.

Brookfield Infrastructure’s Global Reach

Brookfield Infrastructure is a dividend growth stock, with its partnership units yielding 4.8% and corporate shares yielding 3.8%. Over the past decade, Brookfield Infrastructure Partners stock has more than tripled investors’ money, driven by dividend growth. Since its corporate shares were listed in 2020, they have more than doubled investors’ returns with reinvested dividends.

Brookfield Infrastructure’s diversified asset portfolio spans utilities, transportation, midstream energy, and data infrastructure across the Americas, Europe, and Asia-Pacific regions. The essential nature of these assets ensures that 90% of the company’s cash flows are contracted, making them highly predictable and stable.

The company has grown its funds from operations by a compound annual growth rate (CAGR) of 15% and its dividend by 9% CAGR since 2009. Brookfield Infrastructure stands as an intriguing play on significant global trends, such as digitalization and decarbonization. With numerous growth opportunities, the company is confident in expanding its annual dividend by 5% to 9% in the long term. This dividend growth should sustain the stock’s yield, paving the way for potential multibagger returns over the next decade.

A Final Consideration: Investing in Brookfield Infrastructure Partners

Before diving into Brookfield Infrastructure Partners, consider this: The Motley Fool’s Stock Advisor analyst team has identified what they believe are the 10 best stocks for investors to buy now, and Brookfield Infrastructure Partners didn’t make the list. The chosen stocks have the potential to deliver substantial returns in the coming years.

Reflect on when Nvidia was added to this list on April 15, 2005. If you had invested $1,000 at the time of recommendation, it would have grown to $710,860! The Stock Advisor service offers investors a straightforward blueprint for success, including portfolio-building guidance, regular analyst updates, and two new stock picks each month. Since 2002, the Stock Advisor service has more than quadrupled the return of the S&P 500.

Explore the 10 top stocks ›

Stock Advisor returns as of September 17, 2024.